Malaysians are no strangers to skewed agreements. From IPP subsidies to guaranteed profits for highway concessionaires, the public has on numerous times endured the consequences of sheer governmental incompetence.

Yet, the 12-year tax exemption given to Lynas may prove to be the biggest blunder ever.

Lynas is projected to make about AUD 6.2 billion in pre-tax profit in 2012 and 2013 and in exchange, we allow them to contaminate our land for free.

The graph below shows the spectacular rise in rare earth price since Q3 2010. While gold's bull run has been getting plenty of attention of late, the real star is rare earth, which has taken off to astronomical heights.

For Lynas, the price of the rare earths from Mount Weld may increase 15.7 times from JP Morgan's estimate by the time the Lynas Advanced Materials Plant (Lamp) begins production in 2012.

For Lynas, the price of the rare earths from Mount Weld may increase 15.7 times from JP Morgan's estimate by the time the Lynas Advanced Materials Plant (Lamp) begins production in 2012.

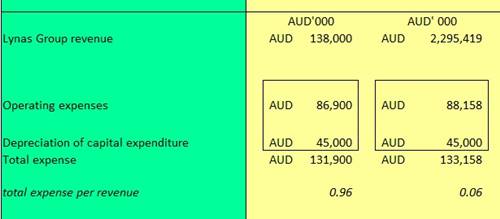

JP Morgan published their stock analysis on 24 June 2010, just prior to the price break out. They have predicted a ridiculously conservative average price of USD 17.69/kg in 2012. At that price, they have expected Lynas to be breaking even in making AUD 4.8 million in net tax profit in 2012. The price has since shot up to USD 201.35/kg on 22 Aug 2011.

Based on linear regression calculated from 3Q10 to 22 August 2011, and extrapolated to 1 January 2012, the price may even surge up to USD278.14.

The following table shows our revised estimates based on JP Morgan's research. We predict Lynas will make AUD 2.2 billion in 2012 and AUD 4.1 billion in 2013 before tax based on the above linear regression estimation (if the 22 August price of USD 201.35/kg is used, 2012 and 2013 profits would be AUD1.5 billion and AUD 2.9 billion respectively).

No matter what the price would be, Lynas will be able to repay their entire setup cost of AUD 807 million and still be able to make super normal windfall profit within the first year. The profit is expected to double up in 2013 when production from Phase 2 commences.

Certain important assumptions are made in this deduction, and they are:

Certain important assumptions are made in this deduction, and they are:

a) The revenue is directly proportional to the increase in rare earth price.

b) Rare earth prices are able to sustain at an average of USD 278.14.13/kg. This is justified by assuming that the downside risk of new supply sources is balanced by the upside risk of China's continual pull back in production.

c) Production of Phase 2, which will double Lamp's capacity to commence production by 2013. Construction of Phase 2 is scheduled for completion by Q4 2012.

d) In 2012 and 2013, the AUD/USD rates are 0.95 (rate at 25/8/2011) and 0.9 respectively.

e) Exchange rate has impact on revenue (since rare earths are priced in USD) and operating cost (25 percent of total operating cost to run the Mount Weld concentration plant is denominated in AUD).

JP Morgan has estimated that the internal transfer price of the semi-refined ores from the Mount Weld concentration plant to its Malaysian subsidiary to be approximately 30 percent of the finished product price. Consequently, from the AUD 6.2 billion pre-tax profit for 2012-2013, only AUD 1.9 billion will be subjected to Australian tax.

The next table shows the estimated tax Lynas is liable for. Taking into account the new Minerals Resource Rent Tax (MRRT), which is effectively levied at 22.5%, Lynas is estimated to pay AUD 683 million in Australian taxes in 2012 and 2013.

However, this amount is small compared to the AUD 2.3 billion in Australian taxes Lynas will have to pay if they have not relocated their plant overseas.

At the prevailing 25% corporate tax rate, Malaysia will be forgoing AUD 1.1 billion or RM 3.4 billion (rates at 25/8/2011) in tax revenue.

There will be some trickledown effects on Lynas' local spending, income tax from Malaysian employees (up to 27 percent) and corporate tax on Lynas' suppliers, but these benefits will be negated by the loss in real estate value and the inevitable depression in tourism.

Let's ponder a moment the underlying principles for granting businesses tax holidays.

Malaysia has numerous tax exemption rulings such as pioneer status, investment tax allowance, agriculture allowance and reinvestment allowance.

These tax legislations are meant for promoted industries or promoted areas to facilitate economic growth and job opportunities in designated sectors or geographical areas (namely Sabah, Sarawak and Eastern Corridor of Malaysia).

Examples of Promoted Industries would be manufacturing and tourism, hence the rapid growth of industrial areas and hotels across Malaysia.

By granting Lynas a tax holiday vis-à-vis other "encouraged" endeavor, is the government keen to promote Grim Reaper factories here?

We are already opposed to the establishment of Lynas' facility here. And to let them reap the huge windfall arising from rare earths' price trend movement while incurring huge and potentially disastrous social cost without making them compensate Malaysians adequately (if at all), shows just too clearly the inability of the present government to administer burden of tax in an equitable manner.

The Australian public would also be denied their rightful share of Lynas' obligation to pay MRRT, should the plant be based in Australia instead hence the present Malaysian government is really presenting an unwitting loop hole to Lynas and doing huge disservices to the population of both nations.

This tax exemption is proving to be the worst agreement the Malaysian government has ever made. At least for other lop-sided agreements, no matter how skewed the terms are, at least there are still some benefits, such as having power and access to highways. But for Lynas, there is absolutely no benefit at all except imminent harm.

The final insult is that the Radiological Impact Assessment (RIA) has indicated that the plant is designed to store only 10 years of waste.

This means that Lynas may have already packed up and gone when their 12 years is up, leaving behind radioactive waste for the locals to deal with.

In conclusion, Malaysia is basically rolling out the red carpet to Lynas to turn our land into a permanent waste depository. It is absolutely illogical. Therefore, we appeal to the government's common sense to stop Lynas from operating.

Note: The assumed operating capacity was not indicated in JP Morgan's report. They may have conservatively assumed that LAMP will only be running at 79 percent of the maximum capacity of 11,000 tonnes (deduced using the forecasted revenue of AUD 138 million divide by rare earth price of USD 17.69/kg).

If this assumption was made, Lynas stands to make AUD 2.8 billion in 2012 and AUD 5.2 billion in 2013 in pre-tax profit at full capacity.

However, it might also be possible that the shortfall in revenue is the result of long term supply contracts at below market rare earth price.

SOO jIN HOU and LEE WEE TAK belong to the Kuantan Environmental Watch Group.